You Earn on a 1099.

You Deserve a Mortgage.

Your write-offs shouldn’t kill your home loan. At Jhenesis Mortgage, we qualify you on what you actually earn — your gross 1099 income — not the reduced number left after deductions. No W-2. No tax return maze. Just your 1099 forms and a clear path forward.

Get Your Free 1099 Pre-Qualification

Takes 2 minutes. No credit pull. No commitment.

Jhenesis Mortgage NMLS #2532705 · Equal Housing Lender

If You Receive a 1099, You May Already Qualify

A 1099 mortgage isn’t just for tech freelancers. It’s built for the full range of how modern professionals earn — and Florida is full of them.

The Rule of Thumb: If the majority of your income comes from 1099 forms — and you’ve been doing it for at least 12 months — you likely have a qualifying pathway through a 1099 mortgage or one of its close cousins (bank statement loan, P&L loan). We help you find the right one.

Core 1099 Mortgage Requirements at a Glance

Income Documentation

1–2 years of 1099-NEC, 1099-MISC, or 1099-K forms. Some lenders accept 12 months if income is stable or trending up.

Credit Score

Minimum 660 for most programs; some lenders require 700+. Strong credit helps offset alternative documentation.

Down Payment

Typically 10–20% for primary homes. Investment properties may require 20–25%. Reserves of 3–12 months PITI are common.

Self-Employment History

Most programs want 2 years in the same field. If you transitioned from W-2 to 1099 at the same company, combined time may count.

Debt-to-Income (DTI)

Target under 43–50%. Unlike conventional loans, DTI is calculated against your gross 1099 income — not your tax return net income.

Income Trend

Stable or increasing income is ideal. Declining income triggers a 12-month average — which may reduce your qualifying amount.

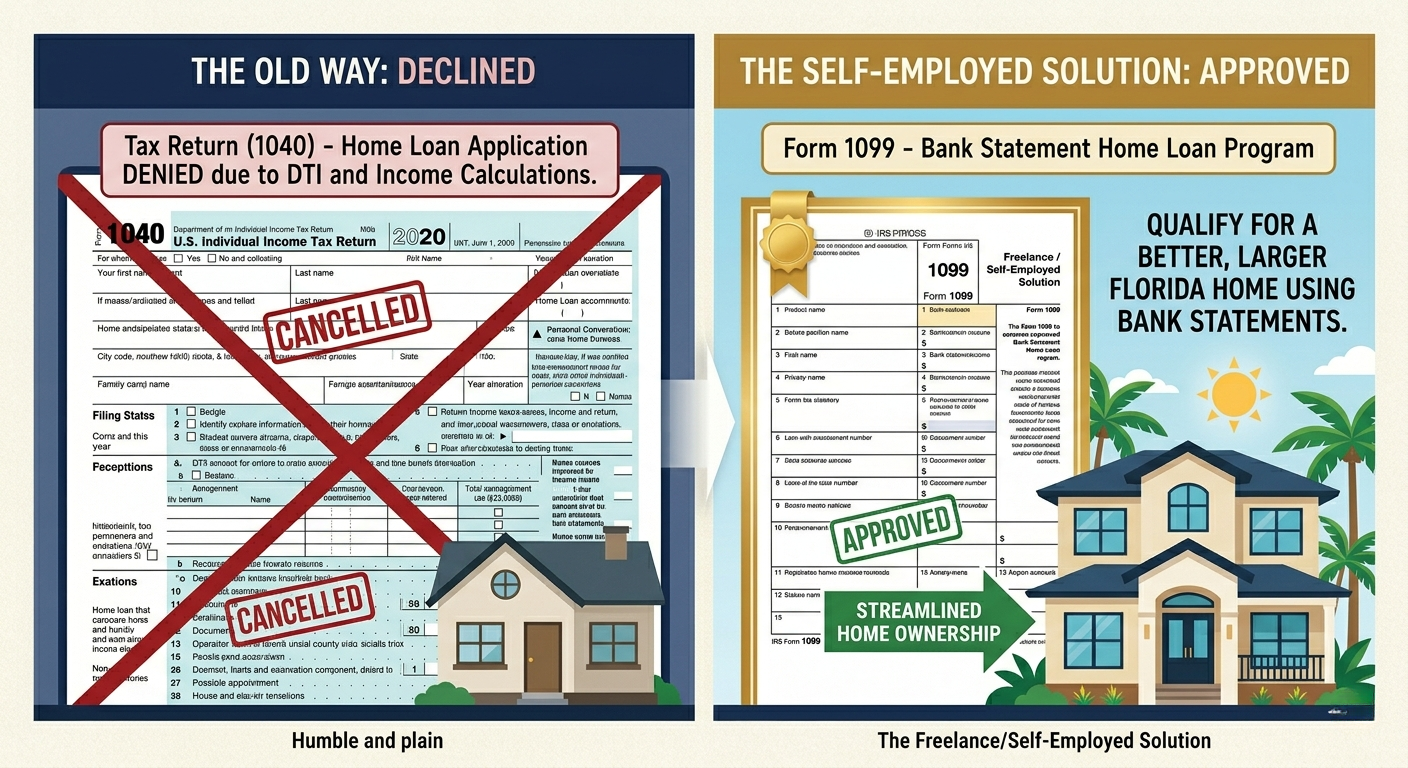

The Write-Off Trap: Why Your Tax Strategy Can Hurt Your Mortgage

Here’s something your CPA may not have told you — and it costs Florida contractors thousands of dollars in buying power every year.

When you write off business expenses on your Schedule C, you reduce your taxable income. That’s smart tax strategy — until you try to buy a home. Traditional mortgage lenders use your tax return net income to calculate what you can afford. The more aggressive your write-offs, the less income your lender sees on paper.

This is what I call the Smart Tax Paradox: you’re doing everything right as a business owner, and it’s punishing you at the mortgage counter.

Nurse Practitioner, Orlando · $132,000 gross 1099

Net income after Schedule C deductions — what a conventional lender uses. Qualifies for roughly ~$280,000 home.

Same Borrower · Same Income

Qualifying income using 90% of gross 1099 ($132,000 × 90%). Qualifies for approximately ~$420,000+ home.

💡 The 1099 mortgage fix: Non-QM lenders use your gross 1099 income — typically 90% of what’s on your forms — before any Schedule C deductions. This one change can add $100,000+ to your buying power without changing a single dollar of your income.

No Tax Return? No Problem.

The self-employed mortgage with no tax return requirement exists specifically because the IRS tax system and the mortgage qualification system use income very differently. Your accountant optimizes for the IRS. Your mortgage broker optimizes for your buying power. The 1099 loan is the bridge between the two.

With a 1099-only mortgage, the income that drives your qualification comes directly from your 1099 forms — gross earnings, before any deductions. Your Schedule C write-offs stay where they belong: on your tax return.

1099 Income Qualifier Calculator

This tool applies the same formula non-QM lenders use: gross 1099 income × 90% expense factor, averaged over 12 or 24 months depending on your income trend. Then it shows your estimated qualifying monthly income and maximum loan range.

No lender does this in real time for 1099 borrowers. Most calculators only handle W-2 income. This one doesn’t.

Your 1099 Mortgage Estimator

Enter your income below for an instant estimate.

Estimate only. Actual loan amounts depend on credit score, reserves, property type, LTV, and lender guidelines. This estimate assumes 30-year term, no HOA or PMI. Speak with a licensed broker for a full qualification review.

↑ Enter your Year 1 income to see your estimate

1099 Loan vs. Bank Statement vs. Conventional: Side-by-Side

Not every 1099 borrower needs the same loan. Here’s how your main options stack up so you can walk into your consultation already knowing the landscape.

| Feature | 1099-Only Loan ✦ | Bank Statement Loan | P&L Only Loan | Conventional/FHA |

|---|---|---|---|---|

| Income Proof | 1099 forms only | 12–24 months bank statements | CPA-prepared P&L | Tax returns + W-2 |

| Tax Returns Required? | ✗ Not Required | ✗ Not Required | ✗ Not Required | ✓ Required |

| Qualifying Income Basis | 90% of gross 1099 | Deposits minus expense factor | Net income on P&L | Net AGI from Schedule C |

| Min. Credit Score | 660+ | 620–660+ | 660+ | 580–620+ |

| Typical Down Payment | 10–20% | 10–20% | 10–20% | 3–3.5% |

| Best For | Contractors, freelancers, agents with clear 1099s | Borrowers with large write-offs & strong deposits | Business owners with organized books | W-2 employees with consistent payroll |

| Rate Premium vs. Conventional | +0.5%–1.5% | +0.75%–2.0% | +0.75%–1.75% | Baseline |

| Investment Property OK? | ✓ Yes | ✓ Yes | ✓ Yes | ✓ Typically |

✦ = Most popular option for borrowers with clean, consistent 1099 history. Guidelines vary by lender.

One Broker Who Knows Both Sides of the Table

I’m Stacy Ann Stephens — a licensed Florida Mortgage Broker and licensed Realtor. After 24+ years working across Connecticut and Florida markets, I’ve seen what happens when 1099 borrowers walk into lenders who don’t understand their income structure. They get turned down — or approved for far less than they actually qualify for.

As a non-QM specialist, I work with a network of wholesale lenders who know exactly how to underwrite 1099 income. I run your numbers through multiple programs, find the one that qualifies you for the most, and stay with your file from application to close.

NMLS #1933745 · Jhenesis Mortgage NMLS #2532705 · Equal Housing Lender

Schedule a Free Strategy Call →

💡 The Buy-Now / Refi-Later Strategy

Many 1099 borrowers use a two-step approach: get into the home today with a 1099 non-QM loan, build 12–24 months of on-time payment history, then refinance into a conventional loan at a lower rate once you have 2 years of tax returns showing qualifying income. The math often works — especially in a Florida market that tends to appreciate.

How the 1099 Mortgage Process Works — Step by Step

The process is simpler than you think. Less paperwork, not more — just the right paperwork.

Free Eligibility Review (15 minutes)

We review your income, credit profile, and goals. You’ll know within one conversation whether a 1099 loan, bank statement loan, or another program is your best route — and a rough number for what you can afford.

Gather Your Documents

For a 1099-only loan, you typically need: 1–2 years of 1099 forms, 2–3 months of bank statements, government ID, and proof of your field (client list, business license, or accountant letter). No tax returns required on most programs.

Income Calculation & Pre-Approval

We calculate your qualifying income using the 90% gross method (or P&L if that’s stronger), run your DTI, and issue a solid pre-approval letter — one that won’t fall apart when an underwriter reviews it.

Shop & Make Offers with Confidence

Your pre-approval covers your true buying power. Whether you’re purchasing a primary home in Central Florida or adding an investment property, you’ll compete like a cash buyer.

Underwriting & Close

Non-QM underwriting is manual — a human reviews your file, not just an algorithm. Typical timeline: 21–30 days. We stay with you every step, translating underwriter questions before they become delays.

Documents Typically Required

Tax returns are NOT required on 1099-only programs.

Income Calculation Formula

Net qualifying income ÷ 12 = Monthly income

Monthly income × DTI limit = Max monthly payment

Max payment → Loan amount at current rate

If using 2 years of 1099s: average both years if income is stable or increasing. Use only the most recent year if income is declining.

1099 Mortgage FAQ

Real answers — the kind that actually help you decide if this loan is right for you.

A 1099 mortgage loan is a type of non-qualified mortgage (non-QM) that allows borrowers to qualify for a home loan using their IRS Form 1099 income — instead of traditional W-2s or tax returns. It’s specifically designed for independent contractors, freelancers, gig workers, and self-employed professionals whose real income isn’t accurately reflected by their tax return after business deductions.

Rather than using net income from Schedule C, 1099 mortgage lenders use 90% of your gross 1099 income to calculate your qualifying amount. This often results in significantly higher buying power for contractors and freelancers who write off substantial business expenses.

Yes. A 1099-only mortgage program is specifically built to qualify borrowers using only their 1099 forms — no W-2, no tax returns required. Lenders calculate your income directly from your 1099 gross earnings, applying a 90% expense factor to arrive at qualifying income.

That said, you’ll still need to show bank statements (typically 2–3 months), proof of self-employment, and meet credit and down payment requirements. The “no tax return” element refers to income verification — other standard mortgage documentation still applies.

The standard 1099 income calculation for mortgage qualification works as follows:

Step 1: Take your total gross 1099 income for the most recent 1 or 2 years.

Step 2: Multiply by 90% (the standard expense factor — this represents 10% assumed expenses).

Step 3: Divide by 12 (or 24 if using two years) to get your monthly qualifying income.

Step 4: Apply your DTI limit to determine maximum monthly payment and loan amount.

Example: $120,000 gross 1099 × 90% = $108,000 ÷ 12 = $9,000/month qualifying income.

If your income is declining year-over-year, lenders will use only the most recent 12 months. If it’s stable or increasing, the 24-month average is typically used. An optional CPA-prepared P&L statement can sometimes be substituted if it results in a stronger qualifying income.

Most 1099 mortgage programs require a minimum credit score of 660. Some lenders set the bar at 700, particularly for lower down payment scenarios. However, credit score requirements can be flexible when compensating factors are present — such as a larger down payment (20%+), strong cash reserves (6–12 months PITI), or stable long-term 1099 income history.

If your score is below 660, a bank statement loan or P&L loan may have slightly more flexibility, or we may recommend a short credit optimization period before applying. We’ll tell you honestly which path makes the most sense for your timeline.

For a primary residence purchase using a 1099 loan, down payment requirements typically range from 10% to 20% depending on your credit score, income stability, and the specific lender’s program. A 10% down payment is possible with stronger credit (720+) and solid income history. A 20% down payment unlocks the best rates and the most program options.

For investment properties financed with a 1099 loan, expect 20–25% down. DSCR loans (qualifying on the property’s rental income rather than your 1099 income) are another powerful option for investors — and may require less documentation overall.

This depends on your specific situation. Most programs want 2 years of 1099 history in the same line of work. However, there are notable exceptions:

W-2-to-1099 transition: If you transitioned from a W-2 position to a 1099 arrangement in the same field — even with the same company — some lenders will combine your W-2 and 1099 history to meet the 2-year requirement, provided the combined period equals 2 years.

12-month programs: Some non-QM lenders (like NASB) accept as little as 12 months of 1099 history under certain conditions. These typically require stronger credit and a larger down payment.

If you’re under 12 months, a bank statement loan or a co-borrower scenario may be your best near-term option. We’ll map out your full picture during your free consultation.

Yes — 1099 mortgage loans are non-QM products, which means they don’t conform to Fannie Mae or Freddie Mac guidelines. As a result, rates typically run 0.5%–2.0% above comparable conventional mortgage rates. In today’s market (mid-2025), this generally translates to rates in the 6.75%–8.50% range depending on your credit score, loan-to-value ratio, and loan size.

That said, rate isn’t the only variable. Many borrowers find that the access to a larger loan amount — possible only because the 1099 loan uses gross income — outweighs the rate premium. Additionally, electing a prepayment penalty (3–5 years) can reduce your rate by 0.375%–0.75%, which makes sense if you plan to stay in the property long-term. We’ll model both scenarios for you.

Both are non-QM mortgage products for self-employed borrowers, but they verify income differently:

1099 loan: Uses your 1099 forms directly. Lenders apply a 90% factor to gross 1099 income. Ideal when your 1099s clearly show your earnings and your business expenses are modest.

Bank statement loan: Uses 12–24 months of personal or business bank statements. Lenders analyze actual deposits and apply an expense factor (often 50% for business accounts, less for personal). Better when your 1099s understate actual income because you collect payments not always reported on 1099s, or when deposits show a stronger picture than your 1099 forms.

The right choice depends on which method produces a higher qualifying income for your specific situation. As your broker, we run both calculations and recommend whichever puts you in the strongest position.

Absolutely — and this is one of the most underserved situations in the mortgage industry. Real estate agents are typically classified as independent contractors and receive 1099-MISC or 1099-NEC income from their brokerages. Because their income is commission-based and fluctuates, conventional lenders often undercount their actual earnings.

A 1099 mortgage is frequently the right fit for agents who have 1–2 strong earning years on record. Because I’m both a licensed Realtor and a licensed Mortgage Broker, I understand exactly how agent income works — the seasonal patterns, the variable deal closings, and how to present your income picture to an underwriter in the strongest possible light.

Yes. 1099 loans are available for primary residences, second homes, and investment properties. For investment properties, expect to put down 20–25% and carry slightly higher rates than primary home financing.

However, if you’re purchasing an investment property as a 1099 earner, a DSCR loan may actually serve you better — particularly if the property will generate rental income. DSCR loans qualify based on the property’s cash flow (rent ÷ mortgage payment), not your personal income at all. This means your 1099 write-offs are completely irrelevant to the qualification process. Many of my investor clients use both: a 1099 loan for the primary home, DSCR for the rental portfolio.