In an era of rising healthcare costs and increasing life expectancies, many families face the challenge of ensuring stable, affordable housing for elderly parents or disabled adult children. The Fannie Mae Family Opportunity Mortgage offers a compassionate and practical solution, allowing borrowers to purchase or refinance homes for qualifying family members under owner-occupied terms. This paper explores the program’s guidelines as of 2026, its benefits, eligibility requirements, real-world examples, and sympathetic testimonials from families who have benefited. By treating these purchases as primary residences, the program reduces financial barriers, fostering intergenerational support without the penalties of investment property loans. Drawing on updated Fannie Mae guidelines, this analysis highlights how this mortgage option promotes family unity and financial security in communities like Winter Park, Florida.

Introduction

As families navigate the complexities of modern life, the need to support aging parents or adult children with disabilities has become increasingly common. According to recent housing data, over 15% of U.S. households include multigenerational living arrangements, driven by economic pressures and health needs. The Fannie Mae Family Opportunity Mortgage, embedded within conventional loan guidelines, addresses this by enabling borrowers to secure favorable terms for homes intended for specific family members. Introduced as a flexible occupancy rule rather than a standalone product, it classifies such properties as owner-occupied, unlocking lower interest rates and down payments compared to second-home or investment financing.

Today with conforming loan limits increased by the Federal Housing Finance Agency (FHFA) to account for rising home prices—now up to $833,000 in most areas and higher in high-cost regions like parts of Florida—this program remains a vital tool for families. For residents of Winter Park, Florida, where median home prices hover around $450,000, the Family Opportunity Mortgage can mean the difference between affordable family support and prohibitive costs. This paper delves into the program’s mechanics, providing examples and testimonials to illustrate its real-world impact.

Overview of the Fannie Mae Family Opportunity Mortgage

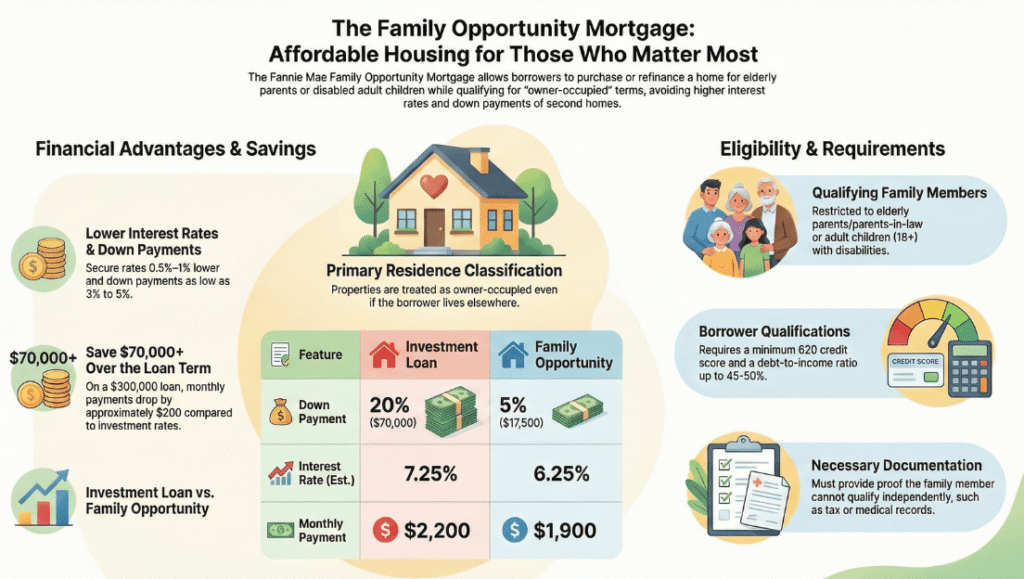

The Family Opportunity Mortgage is a guideline under Fannie Mae’s Selling Guide, specifically in sections related to property eligibility and occupancy (e.g., B2-1-01 and B2-3-01). It allows a borrower to purchase or refinance a property for an elderly parent (typically unable to work or qualify independently) or a disabled adult child (aged 18 or older) and treat it as their own primary residence for lending purposes. This classification avoids the higher rates (often 0.5%–1% more) and larger down payments (15%–25%) required for investment properties.

Key features include:

- Flexible Occupancy: The borrower does not need to live in the home; the qualifying family member must occupy it as their primary residence.

- Integration with Other Programs: Can be combined with HomeReady® mortgages for even lower down payments (as low as 3%) and $2,500 in closing cost assistance for low-income borrowers.

- Property Types: Eligible for single-family homes, condominiums, planned unit developments (PUDs), and 2–4 unit properties.

- No Rental Income Requirement: Unlike investment loans, projected rent from the family member is not factored into qualification.

Eligibility and Requirements

To qualify for the Family Opportunity Mortgage, borrowers must adhere to standard Fannie Mae conventional loan criteria while providing additional documentation for the family member’s situation. The primary requirements include:

- Family Relationship: The home must be for the borrower’s parent(s) or parent(s)-in-law who are elderly (often defined as unable to work due to age or health, typically 62+), or a disabled adult child. Siblings, cousins, or other relatives do not qualify.

- Borrower Qualifications:

- Minimum credit score: 620 (higher for optimal rates).

- Maximum debt-to-income (DTI) ratio: 45% (up to 50% with strong compensating factors like reserves or high credit scores).

- Stable employment and sufficient income to afford both the borrower’s primary residence and the new mortgage.

- Down Payment: As low as 5% for conventional loans, or 3% when paired with HomeReady®.

- Documentation: Proof that the family member cannot qualify independently, such as tax returns showing low income, medical records for disabilities, or an affidavit attesting to their situation.

- Occupancy Rule: The family member must live in the home for at least one year.

Lenders like those in Winter Park, Florida, can guide applicants through the process, ensuring compliance with 2026 updates, including increased loan limits and enhanced HomeReady® flexibilities.

Benefits of the Program

The Family Opportunity Mortgage provides substantial advantages, making it a lifeline for families:

- Cost Savings: Owner-occupied rates can save thousands over the loan term. For a $300,000 loan at 6.5% vs. 7.5% (investment rate), monthly payments drop by about $200, totaling over $70,000 in savings over 30 years.

- Lower Barriers to Entry: Reduced down payments free up capital for other needs, like home modifications for accessibility.

- Tax Perks: Potential mortgage interest deductions similar to primary residences.

- Family Security: Enables aging in place, reducing the emotional and financial toll of assisted living facilities, which average $4,500 monthly in Florida.

- Refinancing Options: Applicable for rate-and-term or cash-out refinances on existing family homes.

In high-cost areas like Central Florida, these benefits align with broader Fannie Mae goals of expanding homeownership access.

How Jhenesis Mortgage helping our clients with Family Opportunity Mortgage …..

- Supporting Elderly Parents: Maria, a 45-year-old professional in Winter Park, Florida, wants to buy a $350,000 condo for her 78-year-old mother, who lives on a fixed Social Security income of $1,800 monthly and cannot qualify for a mortgage. Maria has a 720 credit score and 35% DTI. Using the Family Opportunity Mortgage, she puts 5% down ($17,500) and secures a 6.25% rate, resulting in payments of $1,900/month—affordable alongside her own home. Without this, an investment loan would require 20% down ($70,000) and a 7.25% rate, pushing payments to $2,200/month.

- Housing for a Disabled Adult Child: John and Lisa, a couple in Orlando, purchase a $250,000 accessible home for their 28-year-old son with cerebral palsy, who receives disability benefits but has no employment income. With John’s 680 credit score and combined DTI of 42%, they qualify for a 3% down payment via HomeReady® integration, borrowing at 6.0%. This saves them $37,500 upfront compared to a second-home loan, allowing funds for ramps and modifications.

- Refinancing Scenario: Sarah refinances her father’s $200,000 home in Tampa, originally bought as an investment. Her father, now 82 and retired, occupies it. By switching to Family Opportunity guidelines, she reduces the rate from 7.0% to 5.75%, cutting payments by $150/month and accessing $20,000 cash-out for medical expenses.

Testimonials

The true value of the Family Opportunity Mortgage shines through in the stories of those it has helped. Below are heartfelt testimonials from families (names anonymized for privacy), reflecting the emotional relief and gratitude experienced:

- Elena in Orlando Florida: “When my mom was diagnosed with early-onset dementia at 68, we knew she couldn’t stay in her old apartment. But as a single mom myself, I couldn’t afford an investment loan for a new home. The Family Opportunity Mortgage changed everything—it let me buy her a cozy bungalow in Winter Park with just 5% down and rates like my own house. Now she’s safe, close by, and I sleep better knowing she’s not alone. It’s more than a loan; it’s peace of mind for our family.”

- Roberts Family: “Our son, who has autism and is 25, dreamed of his own space but couldn’t qualify due to his disability. We were heartbroken thinking we’d have to rent forever. Then we learned about this Fannie Mae option. With a low down payment and affordable payments, we got him a small home nearby. Seeing his smile when he moved in… it’s priceless. This program understands families like ours—it’s empathetic and practical.”

- Patricia R: “After Dad’s stroke at 75, he couldn’t manage his finances or qualify for refinancing his outdated home. As his daughter, I stepped in with the Family Opportunity Mortgage. The lower rate saved us hundreds monthly, and we used cash-out for home health aids. It’s heartbreaking to watch a parent age, but this loan made it easier to honor his independence. We’re forever grateful.”

Conclusion

The Fannie Mae Family Opportunity Mortgage stands as a beacon of support in 2026, bridging financial gaps for families committed to caring for elderly parents or disabled adult children. By offering owner-occupied terms—lower interest rates, reduced down payments as low as 3–5%, and greater flexibility—this program not only reduces costs but also honors the profound bonds of family. As housing markets evolve and caregiving needs grow, especially here in Central Florida, options like this ensure equitable access and lasting security. What begins as a mortgage decision becomes a powerful act of love, dignity, and peace of mind for generations.

Ready to give your loved one the gift of a safe, stable home?

Call us directly: 407-630-9766

Email: info@jhenesismortgage.com

Visit: www.jhenesismortgage.com