The Self-Employed Buyer’s Guide to

Getting Approved in Florida

Your tax return says one thing. Your bank account says another. Here’s how to bridge that gap — and actually close on a home.

Why Self-Employed Buyers Face Tighter Scrutiny

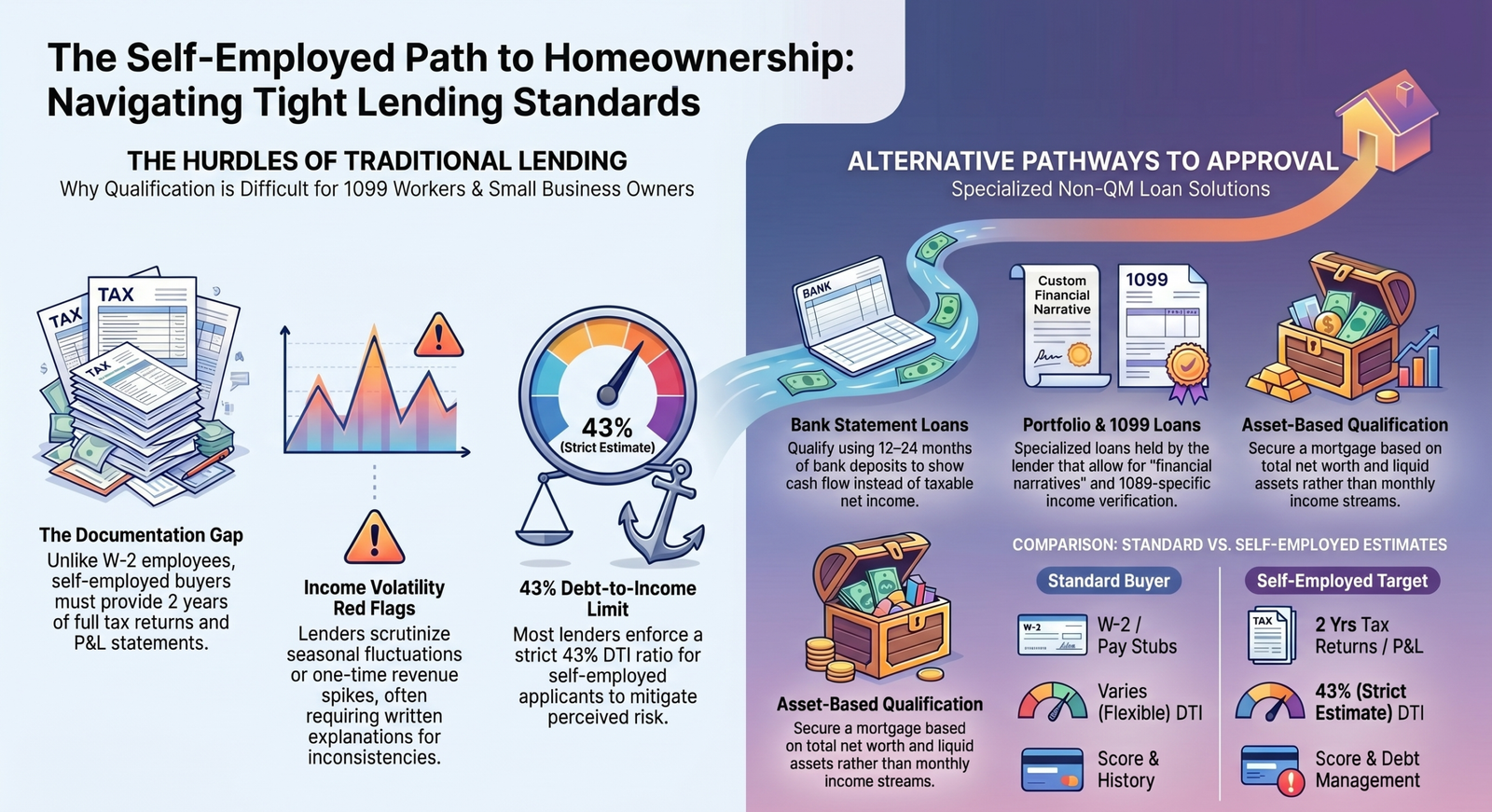

Let me be straight with you: the mortgage system was built around W-2 employees. When you’re self-employed — whether you run a business, work as a 1099 contractor, or freelance — lenders can’t just look at a pay stub and call it a day. They have to work harder to verify your income, and that extra work often comes with extra skepticism.

This isn’t a reflection of your success. I’ve worked with business owners clearing $200K a year who got denied at a traditional bank because their tax deductions made their “qualifying income” look like $60K. That’s the system working exactly as designed — just not in your favor.

After the 2008 mortgage crisis, underwriting standards tightened significantly. Lenders now require documented, verifiable, consistent income over time. Self-employed income is often irregular, heavily deducted on tax returns, or split across multiple entities — which creates friction at every step of the loan process.

Business owners legally minimize taxable income through deductions. But the income lenders use for qualification is often based on that net taxable income — not what actually hit your bank account. The result: you look less qualified than you are.

What Lenders Actually Look At

When you apply for a conventional mortgage as a self-employed borrower, lenders typically look at the following factors — and how to think about each one:

Income Documentation

Traditional lenders want two years of personal tax returns (all schedules), two years of business tax returns (if you have a corporation or partnership), and a year-to-date profit-and-loss statement. They’ll average your Schedule C or Schedule E income across two years — and subtract depreciation and other adjustments. If Year 1 was great and Year 2 was soft, that average may not reflect your current earning power at all.

Debt-to-Income Ratio (DTI)

Lenders compare your monthly debt payments to your gross monthly income. Most conventional programs want your total DTI under 43–45%. If your tax return shows lower income than you actually earn, your DTI ratio looks worse — even if your real finances are solid.

Credit Score

For conventional loans, you generally need a 620+ score. For the most favorable rates, 740+. Self-employed borrowers can be vulnerable here because business debt sometimes gets mixed with personal credit, or because income volatility makes it harder to keep balances low.

Business Longevity & Stability

Most lenders want to see at least 2 years of self-employment history, documented with business licenses, CPA letters, or previous tax returns. A business that’s been running for 18 months, even a profitable one, may not qualify under conventional guidelines.

If you’ve been self-employed for at least 12–24 months and have solid cash flow — even if your tax returns don’t show it — you likely have more mortgage options than you think. The key is using the right loan program for your situation.

Loan Programs That Work for Self-Employed Buyers

This is where most guides gloss over the details. Let me break down each option so you actually understand what it means for your situation.

Bank Statement Loans

Use 12–24 months of personal or business bank deposits instead of tax returns to verify income. Ideal if your deposits are consistent but your Schedule C is full of deductions.

1099 Income Loans

Qualify using your 1099 forms rather than full tax returns. Great for contractors, consultants, and gig workers with consistent 1099 income who’d otherwise be penalized by their deductions.

DSCR Loans

For investment properties — the property’s rental income qualifies the loan, not yours. No tax returns, no W-2s, no DTI calculation. The property pays for itself (or close to it).

P&L Statement Loans

A CPA-prepared profit-and-loss statement (often covering 12–24 months) is used in place of tax returns. Useful if your business is profitable but returns show high deductions.

Asset-Based Loans

Qualify based on your liquid assets — retirement accounts, investment portfolios, savings. Your net worth becomes your qualifier, with no income verification required.

Portfolio Loans

Held by the lender instead of sold to investors, so they can use their own underwriting guidelines. More flexibility, more personalization — and a real conversation about your situation.

Side-by-Side Comparison

Not every loan fits every situation. Here’s a quick look at how the main options compare for self-employed borrowers:

← Scroll to see full table →

| Loan Type | Tax Returns Needed? | Min. Credit Score | Best For | Rate vs Conv. |

|---|---|---|---|---|

| Conventional | Yes (2 yrs) | 620+ | Strong tax return income | Lowest |

| Bank Statement | No | 640+ | High deposits, high deductions | Slightly higher |

| 1099 Loan | No | 620+ | Contractors & consultants | Slightly higher |

| P&L Statement | No | 640+ | Profitable businesses, high deductions | Slightly higher |

| DSCR | No | 620+ | Investment property buyers | Comparable |

| Asset-Based | No | 680+ | High net-worth, lower income shown | Higher |

| Portfolio Loan | Case by case | Varies | Complex or unique situations | Varies |

Quick Affordability Calculator

Get a ballpark on your buying power. This tool uses a 43% DTI estimate — common for non-QM self-employed programs.

* Estimates only. Based on 43% DTI max. Does not account for taxes, insurance, HOA, or exact underwriting. Speak with a licensed mortgage broker for an accurate pre-qualification.

Credit & Documentation Tips

The best thing you can do before applying is get your financial story organized. Here’s what I tell every self-employed buyer who comes to me:

Documentation Checklist for Self-Employed Buyers

- 12–24 months of personal bank statements (all pages, all accounts)

- 12–24 months of business bank statements (if using business deposits)

- Last 2 years of personal tax returns with all schedules (if using conventional or FHA)

- Last 2 years of business tax returns (S-Corp, LLC, Partnership)

- Current-year YTD profit-and-loss statement (CPA-prepared or signed)

- Business license or business registration documents

- 1099 forms from the last 2 years (if using 1099 loan program)

- Photo ID and Social Security Number or ITIN

- Any business license renewals, contracts, or client agreements showing ongoing work

- Letters of explanation for any significant income changes

Protecting and Improving Your Credit

Credit is one of the few factors you can control before applying. A few things that move the needle for self-employed borrowers specifically:

- Keep business and personal credit separate. If your business credit card shows high utilization, it can drag your personal score down. Consider separating them before you apply.

- Don’t open new credit accounts in the 6–12 months before applying. New inquiries and new accounts temporarily lower your score.

- Pay down revolving balances below 30% of each limit. This single move can raise scores by 20–40 points in a billing cycle.

- Dispute any errors. Pull your free reports from AnnualCreditReport.com and review them before a lender does. Errors are more common than most people realize.

Mistakes That Kill Self-Employed Applications

I’ve seen good buyers with solid finances lose deals over preventable errors. Here’s what to avoid:

- Applying at the wrong lender. A big bank with rigid underwriting is not your friend as a self-employed buyer. Work with a broker who has access to non-QM and portfolio lenders.

- Assuming your tax return income is your qualifying income. It might be — but a good mortgage broker will run the math on both your Schedule C or E income AND your bank deposit income to find the most favorable path.

- Large unexplained deposits. Lenders review bank statements carefully. If you received a large transfer, inheritance, or one-time payment, have documentation ready to explain it.

- Inconsistent bank statements. Three months of strong deposits followed by three weak months can raise red flags. Lenders look for a pattern — not a single good month.

- Waiting until you find a house. Get pre-qualified before you start shopping. In a competitive market, sellers won’t wait for you to gather 24 months of bank statements.

- Going it alone. Self-employed mortgage qualification is genuinely complex. A broker who specializes in non-QM lending can often find options a regular loan officer won’t even know to look for.

Frequently Asked Questions

Yes — in many cases. Non-QM bank statement loans and some portfolio programs allow 12 months of self-employment history with strong bank deposits and credit. If you transitioned from W-2 employment in the same field, some conventional programs may also consider a shorter self-employment history. The key is working with a broker who knows which lenders will review your specific situation rather than automatically declining at 24 months.

Typically yes — bank statement loans and non-QM programs carry rates that are 0.5% to 1.5% higher than conventional loans, depending on your credit score, down payment, and the lender. However, many self-employed buyers find that getting approved at a slightly higher rate is far better than not qualifying at all. And as your qualifying situation improves — or rates shift — a refinance is always an option down the road.

It depends on the loan program. Conventional loans start at 3–5% down. Bank statement and non-QM loans often require 10–20% down, depending on the lender and your credit profile. DSCR investment property loans typically require 20–25%. A larger down payment can offset a lower credit score or less-than-perfect income documentation in some programs.

A DSCR (Debt Service Coverage Ratio) loan qualifies based on the rental income a property generates — not your personal income. If a property’s projected rent covers 1.0–1.25x the monthly mortgage payment, it can qualify. No tax returns, no income verification, no employment history required. DSCR loans are specifically designed for real estate investors and are an excellent fit for self-employed buyers who want to build a rental portfolio without the friction of traditional income verification.

Yes — and this is exactly the situation bank statement loans and P&L loans were designed for. If your tax returns show low net income due to legitimate business deductions, but your actual bank deposits tell a different story, a bank statement loan lets lenders evaluate your real cash flow instead. We look at your deposits (personal or business) over 12–24 months, apply an expense factor, and use that as your qualifying income. It’s a much more accurate picture of what you can actually afford.

Yes. Jhenesis Mortgage offers non-QM loan programs for ITIN borrowers and foreign nationals — including self-employed borrowers with international income. ITIN holders can use bank statements from U.S. accounts or, in some cases, international accounts with translated documentation. Foreign nationals purchasing investment property in Florida can use DSCR programs that don’t require any U.S. income documentation at all. Each situation is different, so a direct consultation is the fastest way to map your options.

Typically 21–30 days once all documentation is in hand, which is comparable to conventional loans. The key is getting your bank statements, P&L, and supporting documents organized before you go under contract. Delays almost always come from missing documentation — not from the program itself.