VA Loan Florida 2026: Why Only 15% of Veterans Use This Benefit — and How to Not Miss Out

No down payment. No mortgage insurance. Competitive rates. The VA loan is the most powerful home financing tool in America — and most veterans who earned it aren’t using it.

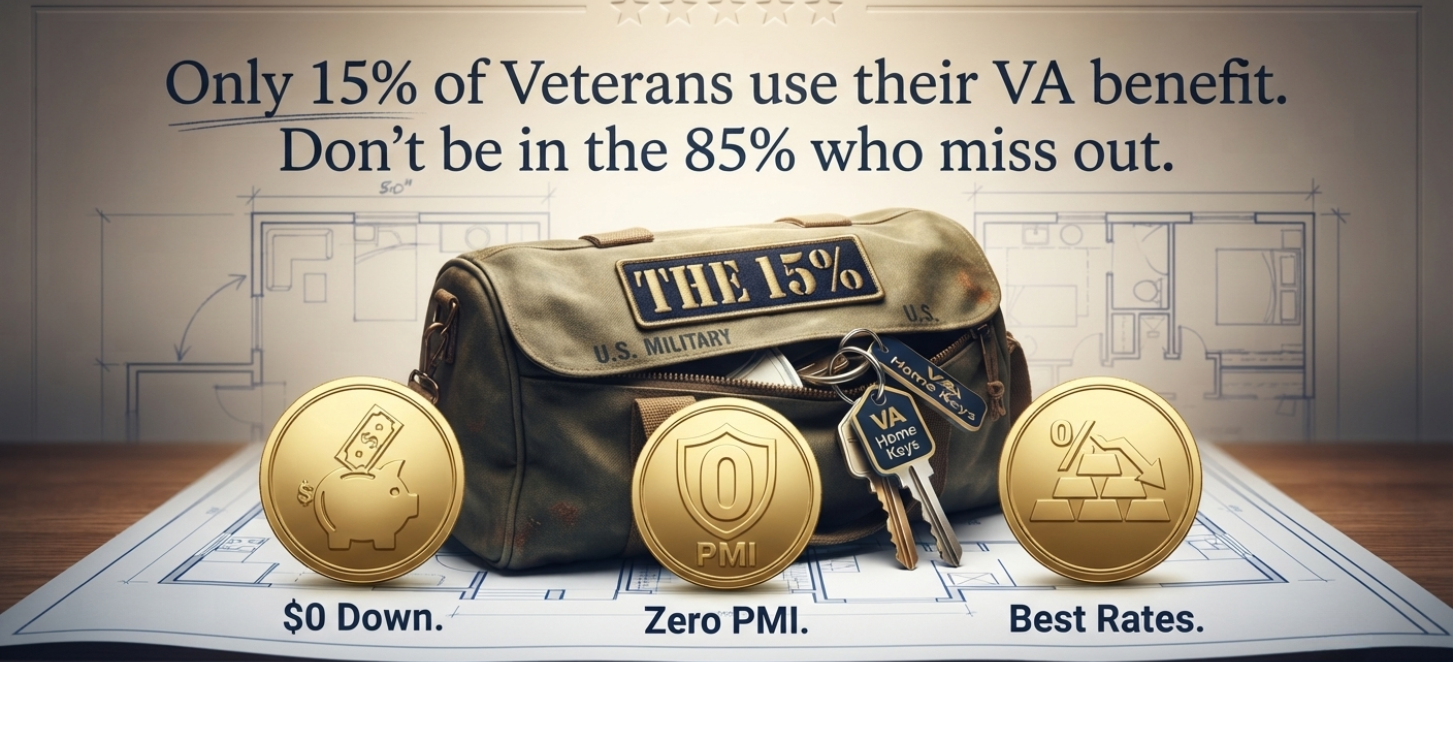

Check My VA Eligibility Free →I went to VA loan training at United Wholesale Mortgage in Detroit, and one statistic stopped me cold: only about 15% of eligible veterans actually use their VA loan benefit. The rest either don’t know they qualify, believe myths about it being harder to use, or were simply never guided toward it.

That number is heartbreaking to me. The VA loan benefit is one of the most powerful homebuying tools in the entire mortgage industry. And it was earned. If you served this country, this benefit belongs to you. Let me make sure you know exactly how it works and how to use it.

That means roughly 85% are leaving one of the best financial tools in existence unused.

What the VA Loan Actually Gives You

| VA Loan Feature | What It Means for You |

|---|---|

| Zero Down Payment | Buy a home without saving years for a down payment |

| No Mortgage Insurance — Ever | No PMI, no MIP — saves $200–$500+/month vs. FHA or conventional with less than 20% down |

| Competitive Rates | VA rates are typically 0.25–0.5% lower than conventional rates |

| No Loan Limit (full entitlement) | Borrow what your income supports — no arbitrary cap for most borrowers |

| Seller Concessions up to 4% | Seller can cover closing costs, prepaid items, and VA funding fee |

| Assumable Loans | A future buyer can assume your rate — a powerful selling point in a high-rate environment |

| Flexible Credit Standards | No official FICO minimum, though most lenders prefer 580–620+ |

| Multiple Uses | Can be used multiple times throughout your life — even simultaneously with remaining entitlement |

| Funding Fee Exemption | Veterans receiving disability compensation are typically exempt from the funding fee entirely |

Who Is Eligible for a VA Loan in Florida?

🎖️ Active Duty Service Members

Eligible after 90 consecutive days of active service during wartime, or 181 days during peacetime.

🎖️ Veterans

Eligible with 90 days active wartime service or 181 days peacetime service. Must be discharged under conditions other than dishonorable.

🎖️ National Guard & Reserve Members

Eligible after 6 years of service, or 90 days of active-duty service under Title 10 federal orders. Many Guard and Reserve members don’t realize they qualify.

🎖️ Surviving Spouses

Unremarried surviving spouses of veterans who died in service or from a service-connected disability are eligible. Spouses of POW/MIA veterans also qualify in certain circumstances.

Share your service history and I’ll help confirm your eligibility before we run any credit. Five-minute conversation — no commitment.

Confirm My VA Eligibility Free →

The VA Funding Fee — What It Is and When You Can Skip It

The VA loan has no monthly mortgage insurance, but it does require a one-time funding fee — typically 1.25%–3.3% of the loan amount, depending on your down payment and whether it’s a first or subsequent use. This fee can be financed into the loan so you don’t pay it out of pocket at closing.

| First Use — Down Payment | Funding Fee |

|---|---|

| Zero down | 2.15% |

| 5% or more | 1.50% |

| 10% or more | 1.25% |

You may be completely exempt from the funding fee if you:

- Receive VA disability compensation for a service-connected disability

- Have a proposed or memorandum VA disability rating

- Are a surviving spouse of a veteran who died from a service-connected disability

- Are a Purple Heart recipient on active duty

If you’re receiving any VA disability compensation, verify your exemption status before closing — it can save you thousands of dollars.

🎖️ VA vs. Conventional Savings Calculator

See how much you save monthly and over 5 years by using your VA benefit instead of a conventional loan with a down payment and PMI.

*Includes VA funding fee (2.15%, first use, financed into loan) vs. conventional PMI estimated at 0.7% annually on the loan amount. Rates are estimates. Actual savings vary. Contact Jhenesis Mortgage for a personalized VA comparison. NMLS #2532705.

5 Myths About VA Loans That Keep Veterans From Using Their Benefit

“VA loans are harder for sellers to accept.”

False — in 2026. A fully approved VA buyer is just as strong as a conventional buyer. The VA appraisal has slightly stricter property standards (the home must meet Minimum Property Requirements), but these standards protect the veteran, not create a burden for the seller. An experienced listing agent and Realtor know this. Your offer should be written as competitively as any other.

“You can only use a VA loan once.”

False. VA entitlement can be restored and reused. Many veterans use VA loans multiple times throughout their lives. With full entitlement — meaning no existing VA loan — you can purchase again with no limit on loan amount. With partial remaining entitlement, a bonus entitlement calculation applies. Selling your previous VA-financed home and paying off the loan typically restores full entitlement.

“VA loans take too long to close.”

Partially false. VA loans do require a VA appraisal by a VA-approved appraiser, which can add a few days compared to conventional. But with a prepared file and an experienced VA lender, VA loans close in 21–30 days — fully comparable to FHA and many conventional loans. The key is choosing a lender who actually knows the VA program and doesn’t treat it like a specialty item.

“The VA funding fee makes it not worth it.”

Almost always false. Even with the 2.15% funding fee financed in, the absence of PMI typically saves veterans $200–$600 per month versus a conventional loan with less than 20% down. That monthly saving typically recoups the funding fee within 24–36 months. Over a 5-year ownership period, total VA savings commonly exceed $15,000–$25,000. And veterans with any disability rating pay zero funding fee.

“Bad credit means I can’t qualify for a VA loan.”

False. The VA has no official minimum credit score requirement. Individual lenders set their own minimums, typically 580–620. The VA’s DTI guidelines are also more flexible than conventional underwriting, especially when the residual income test is met. I’ve helped veterans with credit challenges get approved when they were told elsewhere it wasn’t possible. The program was designed with real flexibility intentionally.

Frequently Asked Questions — VA Loans Florida 2026

You Earned This Benefit. Let’s Make Sure You Use It.

If you served, your first homebuying conversation should start with your VA benefit — not conventional or FHA. No down payment. No PMI. A better rate. Let’s confirm your eligibility and run the numbers together.

Book My Free VA Loan Review →

Stacy Ann Stephens | Mortgage Broker | NMLS #1933745 | Jhenesis Mortgage NMLS #2532705

407-630-9766 | stacyann@jhenesismortgage.com | JhenesisMortgage.com

Informational purposes only. Not a commitment to lend. VA loan eligibility, terms, and funding fee amounts are subject to VA guidelines and lender requirements. Not all borrowers qualify. Contact Jhenesis Mortgage for current VA program details.