Rates are moving. Get your DSCR scenario reviewed before your next deal.

Lock My Rate Now →DSCR Loans Right Now: What Rate Volatility Means for Florida Investors (And When to Lock)

The market is swinging. Tariffs are doing things nobody predicted. Mortgage rates are moving up, then down, then up again — sometimes within the same week. Here’s what that actually means for your next Florida investment property, and the exact framework I’m using with my investors right now.

I want to start with something most lenders won’t say out loud: nobody knows exactly where rates are going. Not the Fed. Not the bond market. Not the economists on CNBC. Anyone who tells you they do is selling something — and it’s not a mortgage.

What I can tell you is what’s causing the volatility right now, what the current numbers look like for DSCR loans in Florida, and the decision framework I actually use with my investors to figure out whether to lock today or wait.

That’s what this post is — the real insider view, not a rate sheet disguised as content.

What’s Actually Moving Mortgage Rates Right Now

DSCR loan rates don’t live in a vacuum. They follow the 10-year Treasury yield, which in turn responds to every macro signal the market gets — inflation data, Fed commentary, employment numbers, and increasingly, trade policy uncertainty.

Here’s the honest picture as of May 2026: tariff announcements from the White House have been creating sharp, unpredictable swings in bond markets. When trade tensions spike, investors flee to Treasuries (safe haven buying), which pushes yields down and mortgage rates with them. When tariff fears ease, that flight reverses, yields rise, and rates follow. We’ve seen this cycle repeat several times in the past two months.

The Fed held rates at its May 2026 meeting — no cuts, no hikes. That’s important context: the Fed’s benchmark rate affects short-term credit costs (like HELOCs and credit cards) more than 30-year mortgage rates. Long-term rates are set by the bond market’s read on inflation and growth, not the Fed directly. So even a Fed cut in late 2026 — which markets are now pricing in for Q4 — wouldn’t automatically bring DSCR rates down. It depends entirely on what happens to inflation data between now and then.

The investors who win in volatile markets aren’t the ones who perfectly time the rate. They’re the ones who run the numbers at today’s rate and know their deal still works.

What Today’s DSCR Rates Mean for Your Florida Deal

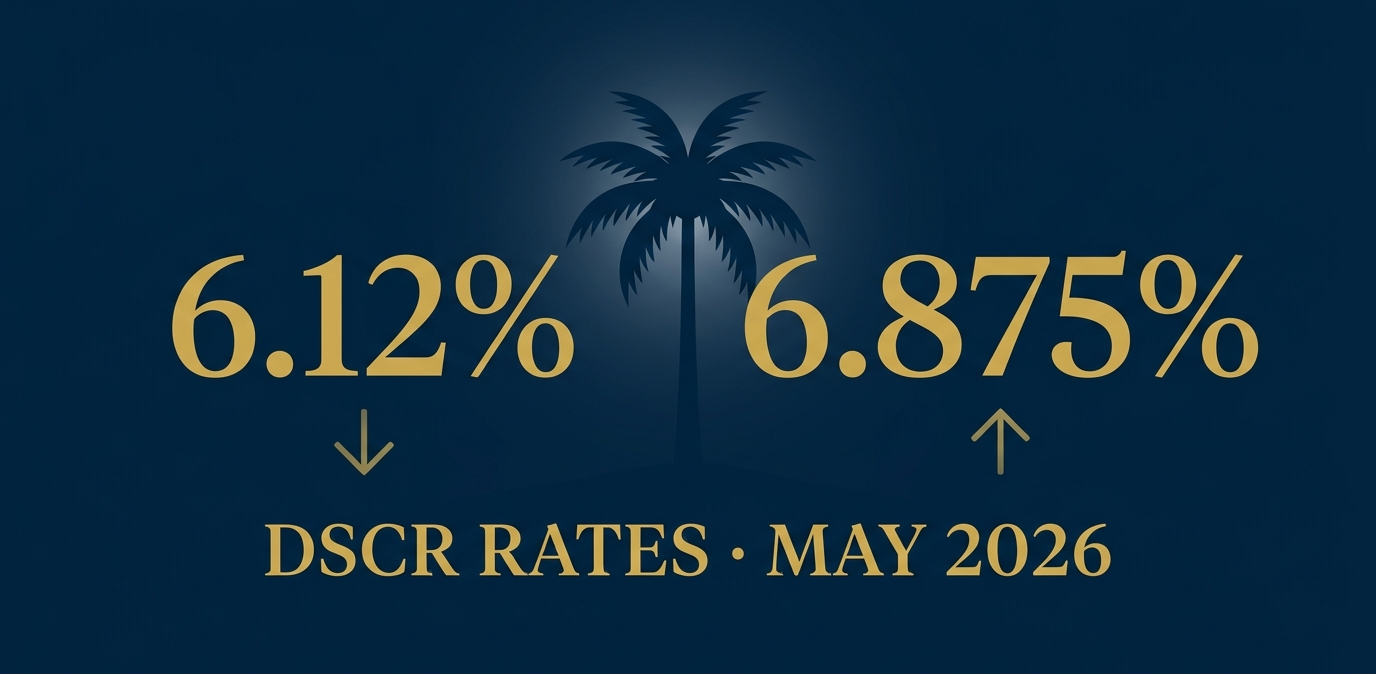

Let’s make this practical. At the current par rates — 6.12% for domestic investors, 6.875% for foreign nationals — here’s what the math looks like across typical Central Florida investment price points.

Remember: DSCR qualification is based on your property’s income, not your personal income, W-2s, or tax returns. The core formula is simple — your gross monthly rent ÷ your monthly PITI payment. A DSCR of 1.0 means the property breaks even. Most lenders want 1.0 to 1.25 minimum.

| Scenario | Purchase Price | 25% Down | Rate | Monthly P&I | Rent Needed (1.15x) |

|---|---|---|---|---|---|

| Domestic — Entry LTR | $350,000 | $87,500 | 6.12% | ~$1,600 | ~$2,100/mo |

| Domestic — Mid Market | $500,000 | $125,000 | 6.12% | ~$2,285 | ~$2,950/mo |

| Domestic — STR | $650,000 | $162,500 | 6.50%* | ~$3,075 | ~$3,970/mo (or STR AVM) |

| Foreign National | $400,000 | $100,000 | 6.875% | ~$1,972 | ~$2,550/mo |

| Foreign National — STR | $550,000 | $137,500 | 7.25%* | ~$2,815 | ~$3,640/mo (or STR AVM) |

*STR and higher LTV scenarios typically carry a rate premium above par. Estimates only — contact for current pricing on your specific scenario. Does not include taxes, insurance, or HOA.

The question isn’t just whether you can qualify. It’s whether the deal works at today’s rate. And that depends on your market, your property type, your down payment, and how you define “works.”

The Rate Lock Decision: When to Lock, When to Float

This is the question I get almost daily right now. And the answer isn’t “always lock” or “always float” — it’s about your timeline, your deal math, and your risk tolerance. Here’s the framework I actually walk through with every investor client.

Lock Now If…

-

You’re closing within 30–60 days and the deal works at today’s rate. Certainty has real value when you have a contract in hand.

-

A 0.25–0.5% rate increase would flip your DSCR below 1.0 and kill the deal’s cash flow. Don’t gamble on a tight deal.

-

You’re a foreign national investor with a longer lock available. Rate premium is already baked in — locking protects against further widening.

-

There’s a macro event on the calendar — Fed meeting, major jobs report, tariff announcement — in the next 30 days. Volatility windows are predictable; so is the risk of floating through one.

Float If…

-

You’re still in the search phase — no contract yet, closing is 90+ days out. You can’t lock until you have a property anyway, and a lot can change.

-

Your DSCR is comfortably above 1.25 and the deal works even at a rate 0.5% higher than today. You have real cushion — floating costs you little.

-

There’s a meaningful near-term catalyst for rates to drop — like tariff tensions escalating, sending bond yields lower. Not guaranteed, but worth watching.

| Situation | Decision | Why |

|---|---|---|

| Contract signed, closing in 45 days, DSCR = 1.12 | Lock | Deal is tight. Rate spike = broken deal. Lock the certainty. |

| Still searching, budget up to $500K, no contract | Float | Can’t lock without a property. Monitor weekly. |

| Contract, closing in 30 days, DSCR = 1.35 | Float or Lock | Cushion exists. Could float but confirm with broker first. |

| Foreign national, closing in 60 days | Lock | FN rate premium can widen fast. Lock while you have it. |

| Refinancing existing rental, no timeline pressure | Float | No closing deadline. Set a target rate and monitor. |

What My Florida Investors Are Actually Doing Right Now

Here’s the real-world picture from my pipeline over the past 30 days:

The locked-in group — investors with contracts in the $350K–$600K range, primarily on LTR properties in Orange, Osceola, and Polk counties, are locking. Their DSCR numbers work at 6.12% and they don’t want to find out what happens if rates spike before closing. The certainty is worth more than the potential savings of floating.

The floating group — investors still in the search phase, particularly Caribbean and Canadian buyers looking at STR properties in Kissimmee and the Space Coast, are floating. They can’t lock without a contract anyway, and the STR income potential on their target properties is strong enough that a 0.25% rate move doesn’t change the fundamental deal quality.

The portfolio refinance group — investors with existing rental properties sitting on pandemic-era rates above 7.5% are watching closely. If we get a meaningful rate drop before year-end, there’s a refinancing wave coming. I’m helping several clients model out their break-even timeline now so they can move fast when the window opens.

The best deal isn’t the one with the lowest rate. It’s the one you actually closed — at a rate that worked — while everyone else was waiting for perfect.

DSCR Rate Lock Breakeven Calculator

Should you lock your DSCR rate today — or float and hope for a dip? Enter your deal numbers and find out exactly when locking pays off.

Frequently Asked Questions About DSCR Loans & Rate Volatility

What is a DSCR loan and how does it qualify differently from a conventional mortgage?

A DSCR loan (Debt Service Coverage Ratio loan) qualifies the borrower based on the investment property’s rental income rather than the borrower’s personal income, W-2s, or tax returns. The DSCR ratio is calculated by dividing the property’s gross monthly rent by the monthly principal, interest, taxes, and insurance (PITI) payment. A DSCR of 1.0 means the rental income exactly covers the mortgage payment; 1.25 means the property generates 25% more income than the payment. Most DSCR lenders require a minimum ratio of 1.0 to 1.25. This structure makes DSCR loans ideal for self-employed investors, foreign nationals, and anyone whose tax returns understate their actual income.

What are current DSCR loan rates in Florida as of May 2026?

As of May 2026, the baseline par rate for DSCR loans in Florida is approximately 6.12% for domestic U.S. investors and 6.875% for foreign national investors, on 30-year fixed-rate structures with a DSCR of 1.0 or higher. Short-term rental (STR) properties and higher loan-to-value scenarios typically carry a rate premium above these par rates. Rates are currently experiencing meaningful volatility driven by tariff-related uncertainty in bond markets — checking current pricing weekly is strongly recommended. These rates reflect par pricing and your actual rate may vary based on credit score, LTV, property type, and lender guidelines.

Why are DSCR mortgage rates volatile in 2026? What is causing the swings?

DSCR mortgage rates track the 10-year U.S. Treasury yield, which is primarily driven by inflation expectations and economic growth signals. In 2026, the primary source of rate volatility has been tariff policy uncertainty. When trade tensions escalate, investors move money into U.S. Treasury bonds as a safe haven, increasing demand and pushing yields — and mortgage rates — down. When tensions ease, that capital rotates back out of bonds, yields rise, and mortgage rates increase. This cycle has repeated several times in Q1–Q2 2026, creating swings of 0.25–0.5% within short windows. Additionally, the Federal Reserve has held its benchmark rate steady in 2026, which has limited downward pressure on long-term mortgage rates even as inflation has moderated.

Should I lock my DSCR rate now or wait for rates to drop?

The decision to lock or float depends on three factors: your timeline, your deal margin, and your risk tolerance. If you have a signed purchase contract and are closing within 45–60 days, and the deal’s DSCR works at today’s rate, locking provides certainty that a rate spike won’t kill your deal. If your DSCR is tight — below 1.15 — a 0.25% rate increase could flip your deal to a break-even or loss. In that case, locking is typically the safer choice. If you’re still in the property search phase with no contract, you cannot lock a rate yet — rates are tied to specific loan applications and properties. In that case, monitoring the market and having a pre-approved scenario ready to move quickly is the best strategy.

Can foreign national investors get DSCR loans in Florida?

Yes. Foreign national investors can access DSCR loans for Florida investment properties without a U.S. Social Security number, U.S. credit history, or U.S. income documentation. Foreign national DSCR loans typically carry a rate premium of 50–100 basis points above domestic investor rates — as of May 2026, the baseline par rate for foreign nationals is approximately 6.875% compared to 6.12% for domestic investors. Lenders evaluate the property’s income-generating ability, not the borrower’s personal financial profile. Down payment requirements for foreign nationals are typically 25–30% for standard properties and may be higher for short-term rental (STR) properties or larger loan amounts. Note: Florida’s SB 264 restrictions apply to certain nationalities — consultation with a qualified attorney is recommended for buyers from affected countries.

What DSCR ratio do I need to qualify for a Florida investment property loan?

Most DSCR lenders require a minimum ratio of 1.0 to 1.25, depending on the lender and the property type. A DSCR of 1.0 means the property’s rental income exactly covers the mortgage payment (principal, interest, taxes, and insurance). Some lenders offer “No-DSCR” or “DSCR below 1.0” programs for investors who accept a slightly higher rate in exchange for qualifying without meeting the standard ratio — these are useful for investors with strong reserves or who are purchasing in high-appreciation markets where long-term equity growth is the primary strategy. For short-term rental properties, many lenders use an AVM (Automated Valuation Model) for projected rental income rather than actual lease agreements, since STR income is variable by season.

Do DSCR loans require tax returns or W-2s?

No — DSCR loans do not require tax returns, W-2s, or personal income documentation. This is their defining characteristic and primary advantage for investors. Qualification is based entirely on the subject property’s rent-to-payment ratio. This makes DSCR loans particularly powerful for self-employed investors, business owners whose tax returns show significant write-offs that reduce their stated income, and foreign nationals who have no U.S. income to document. A lease agreement (for long-term rentals) or a market rent AVM (for short-term rentals) is the primary income documentation required.

How does the Federal Reserve’s rate decision affect DSCR loan rates?

The Federal Reserve’s benchmark rate (the federal funds rate) primarily influences short-term interest rates such as credit card rates, home equity lines of credit, and adjustable-rate mortgages. It has a more indirect effect on 30-year fixed mortgage rates, including DSCR loans. Long-term mortgage rates are primarily set by the bond market’s expectations about future inflation and economic growth — reflected in the 10-year Treasury yield. The Fed held rates steady at its May 2026 meeting. Even if the Fed cuts rates later in 2026, as bond markets are pricing in, 30-year DSCR loan rates may not fall proportionally — it depends on whether long-term inflation expectations also decline. Investors should not assume that a Fed rate cut will automatically deliver lower DSCR pricing.

Let’s Talk About Your Next Florida Investment Deal

Rates are moving. The right move depends on your specific numbers — not a blanket forecast. Book a free 20-minute scenario call and I’ll tell you exactly where your deal stands today.

Stacy Ann Stephens | Mortgage Broker | NMLS #1933745 | Jhenesis Mortgage NMLS #2532705

Rate information is for illustrative purposes only and subject to change without notice. All loan programs subject to credit approval, property eligibility, and lender guidelines. This is not a commitment to lend. Equal Housing Lender.

This content is for informational and educational purposes only and does not constitute financial or investment advice. Consult with a licensed mortgage professional for personalized guidance.