Is an FHA Streamline Refinance Right for You?

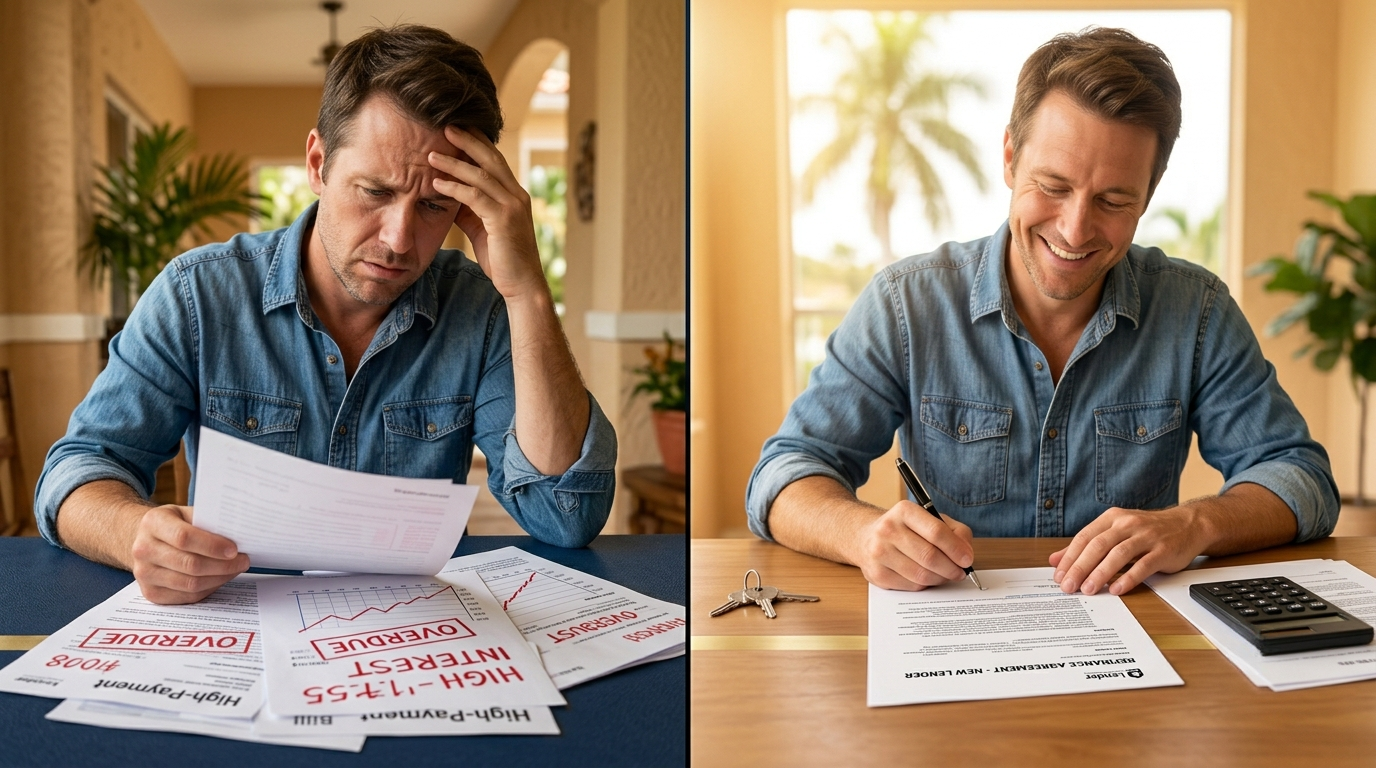

What if you could lower your monthly mortgage payment — without a new appraisal, without re-proving your income, and without six weeks of paperwork? That’s exactly what an FHA Streamline Refinance was designed to do.

If you bought your home with an FHA loan when rates were higher — or if you’re carrying a rate from the last few years that you know isn’t the best available — there may be a faster, simpler path to relief than you think. The FHA Streamline program exists specifically for borrowers who are already in an FHA loan and want to lower their rate or payment with minimal friction.

I’ve walked a lot of clients through this process, and the first thing I tell them is this: this isn’t a standard refinance. It’s designed to be streamlined — fewer documents, less underwriting, no appraisal required in most cases. But “simpler” doesn’t mean “automatic.” There are rules, and knowing them upfront saves you time and frustration.

Let’s break down exactly what the FHA Streamline Refinance is, who qualifies, what it costs, and how to decide if now is the right time to move forward.

What Is an FHA Streamline Refinance — and Why Is It Different?

The FHA Streamline Refinance is a government-backed refinance option exclusively for homeowners who already have an FHA-insured mortgage. It’s called “streamline” because the FHA intentionally reduced the documentation and underwriting requirements compared to a conventional refinance.

Here’s what makes it different from a standard refinance:

- No appraisal required in most cases — your current loan balance is used as the basis, not a new home valuation

- No income verification in a non-credit-qualifying streamline — your DTI isn’t recalculated

- Simplified credit review — most lenders look for 12 months of on-time mortgage payments, not a full underwrite

- Faster closings — because less documentation means less processing time

There are two versions: a non-credit-qualifying streamline (no income docs, no credit score pull in most cases) and a credit-qualifying streamline (used when adding or removing a borrower, or when the lender requires it). Most borrowers go the non-credit-qualifying route.

Key Point: An FHA Streamline Refinance cannot be used to take cash out of your home’s equity. It is a rate-and-term refinance only. If you need cash out, a different refinance product would be more appropriate — and I’m happy to discuss your options.

Ready to see if you qualify?

Takes less than 3 minutes. No obligation, no hard pull on your credit.

Check My FHA Streamline Eligibility →Who Qualifies for an FHA Streamline Refinance

The FHA sets clear eligibility rules, and a good broker will check every one before recommending you move forward. Here are the primary requirements:

1. Your Current Loan Must Be FHA-Insured

This is the non-negotiable starting point. You must already have an FHA loan. If your current mortgage is conventional, VA, or USDA, an FHA Streamline is not available to you — but other refinance options may be.

2. You Must Have Made At Least 6 Payments

The FHA requires that at least 210 days have passed since your first FHA loan payment was due, AND you must have made at least 6 monthly payments. You cannot streamline a brand-new loan.

3. Your Payment History Must Be Clean

For a non-credit-qualifying streamline, you’ll need no more than one 30-day late payment in the past 12 months, and none in the past 3 months. This is the FHA’s way of confirming you’re a responsible borrower even without a full credit check.

4. The Refinance Must Provide a “Net Tangible Benefit”

This is the rule that catches people off guard. The FHA requires your refinance to actually benefit you — typically defined as a reduction of at least 5% in your combined principal, interest, and MIP payment. If the new loan doesn’t meaningfully lower your payment or improve your loan terms, the FHA won’t approve it. This protects borrowers from unnecessary refinancing.

5. You Cannot Be Delinquent on Your Current FHA Loan

Borrowers who are currently behind on their mortgage are not eligible for a streamline refinance. Catching up first and then refinancing is the correct sequence.

Pro tip from Stacy: One thing I always tell clients is to check whether their current FHA loan was originated before June 1, 2009. If it was, you may qualify for a significantly reduced annual MIP rate — which could make the FHA Streamline even more valuable for older loans.

The Real Costs of an FHA Streamline Refinance

Here’s where I want to be fully transparent with you — because this is the part some brokers gloss over. An FHA Streamline Refinance is not free. You will encounter some version of the following costs:

Upfront MIP (Mortgage Insurance Premium)

FHA loans carry mortgage insurance. On a streamline refinance, the upfront MIP is 1.75% of the new loan amount — but here’s the good news: you typically receive a credit for any unexpired upfront MIP from your original loan if it was less than 3 years old. This can significantly offset the cost.

Annual MIP

You’ll also continue paying annual MIP (typically 0.55% to 0.85% of the loan balance, depending on your loan term and amount). If your current loan has a higher MIP rate, refinancing can help reduce this too.

Lender Fees and Closing Costs

Typical closing costs on an FHA Streamline run between 2% and 3% of the loan amount. Lenders are allowed to roll these into the loan — but watch your loan balance carefully. You’re not allowed to increase your loan balance by more than what’s needed to cover allowable closing costs.

Options for Covering Costs

- Lender credits — accept a slightly higher rate in exchange for the lender covering your closing costs (often called a “no-closing-cost” streamline)

- Roll costs into the loan — increase your balance slightly within FHA guidelines

- Pay upfront — if you have the funds and want the cleanest outcome

Let me run your actual numbers

Every situation is different. I’ll tell you exactly what this will cost, what you’ll save, and whether it makes sense for you.

Call (407) 630-9766 for a Free Rate Review🧮 FHA Streamline Savings Calculator

See your estimated monthly savings and break-even point instantly

Estimates are based on principal & interest only and do not include MIP, taxes, or insurance. For a complete analysis, contact Jhenesis Mortgage.

Is Right Now the Right Time to Refinance?

The honest answer: it depends on where you got in and where rates are today. But I want to give you a framework that’s more useful than “wait for rates to drop.”

The Break-Even Rule

The most important number in any refinance decision is your break-even point — how many months it takes your monthly savings to recover the cost of refinancing. Use the calculator above to find yours. If you plan to be in the home longer than your break-even period, refinancing likely makes sense.

The Half-Point Rule of Thumb

As a general guide, a reduction of at least 0.5% in your interest rate is often worth refinancing — especially when paired with FHA’s no-appraisal benefit. That said, the math matters more than the rule. I’ve seen 0.375% reductions that made sense for clients planning a long stay, and 1% drops that didn’t pencil out for someone moving in two years.

What I’m Seeing in the Market Right Now

FHA rates have shown meaningful movement in 2025. Borrowers who financed at 7.25%–8% in 2023 and 2024 may find today’s rates significantly more favorable. The streamline process is faster than ever, and because there’s no appraisal, even borrowers in markets with flat or declining home values can refinance without worrying about equity.

The bottom line: if you’re in an FHA loan and haven’t reviewed your rate in the last 18 months, you’re likely leaving money on the table. A 15-minute call with me can tell you exactly where you stand.

Frequently Asked Questions

In most cases, no. One of the biggest advantages of the FHA Streamline Refinance is that it typically does not require a new home appraisal. Your existing loan balance is used as the basis for the refinance rather than a fresh market valuation. This makes the process faster, less expensive, and available to homeowners regardless of current home value — unlike conventional refinances that require sufficient equity.

Savings vary by loan balance, the difference between your current and new rate, and remaining term. On a $280,000 loan, dropping from 7.25% to 6.25% on a 30-year term saves approximately $175/month — or $2,100 per year. Over 5 years, that’s over $10,000 in savings. Use the calculator on this page for your personalized estimate, or call us for a full breakdown including MIP adjustments.

No. The FHA Streamline Refinance is a rate-and-term refinance only. It is not designed for cash-out purposes. If you want to access your home’s equity, you would need an FHA Cash-Out Refinance or a different product. An FHA Cash-Out Refinance allows you to borrow up to 80% of your home’s current appraised value — but it does require a full appraisal and income documentation.

You must wait at least 210 days from your first FHA loan payment due date AND have made a minimum of 6 monthly payments before you’re eligible. For example, if your first payment was due February 1, 2024, the earliest you could close an FHA Streamline would be around September 2024 — provided all other qualifications are met.

The FHA requires your refinance to deliver a meaningful financial improvement. For fixed-to-fixed rate refinances, you typically need at least a 5% reduction in your combined principal, interest, and MIP payment. For example, if your current P&I + MIP total is $2,000/month, your new payment must be $1,900 or less to meet the net tangible benefit requirement. This rule protects homeowners from refinancing into worse terms.

In a non-credit-qualifying streamline, there is typically no hard credit inquiry, so your credit score is not directly impacted during the approval process. However, the new loan will appear on your credit report as a new account, which may cause a small temporary dip. Over time, consistent on-time payments on the new loan will benefit your credit score. For a credit-qualifying streamline, a credit pull is required.

Let’s Run Your Numbers — For Free

I’ll tell you exactly what an FHA Streamline could save you, what it will cost, and whether the timing is right. No pressure, no obligation — just real numbers from a licensed broker who’s done this for 24 years.

Ready to lower your FHA payment? It takes less than 3 minutes.

Apply Now →